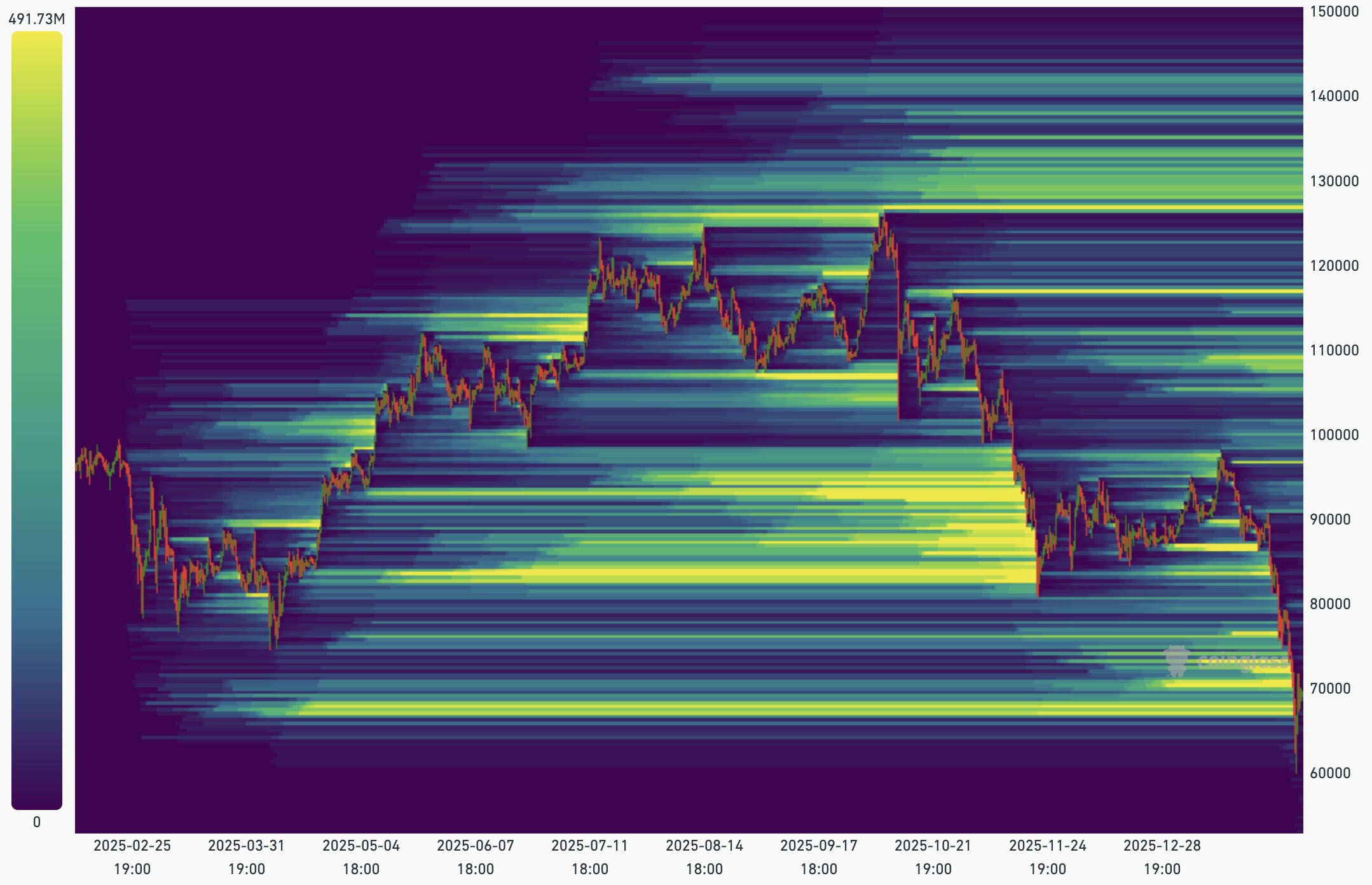

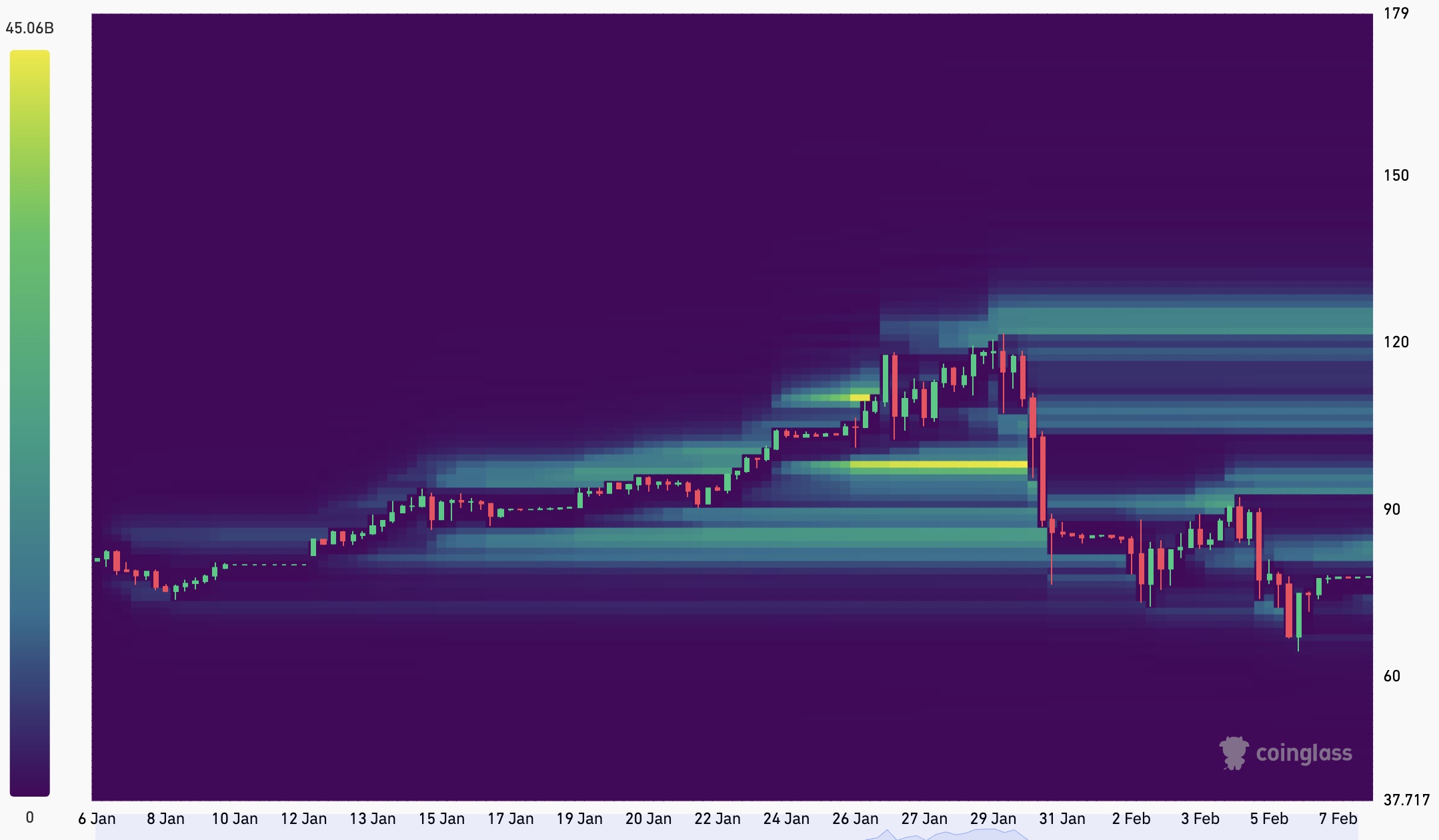

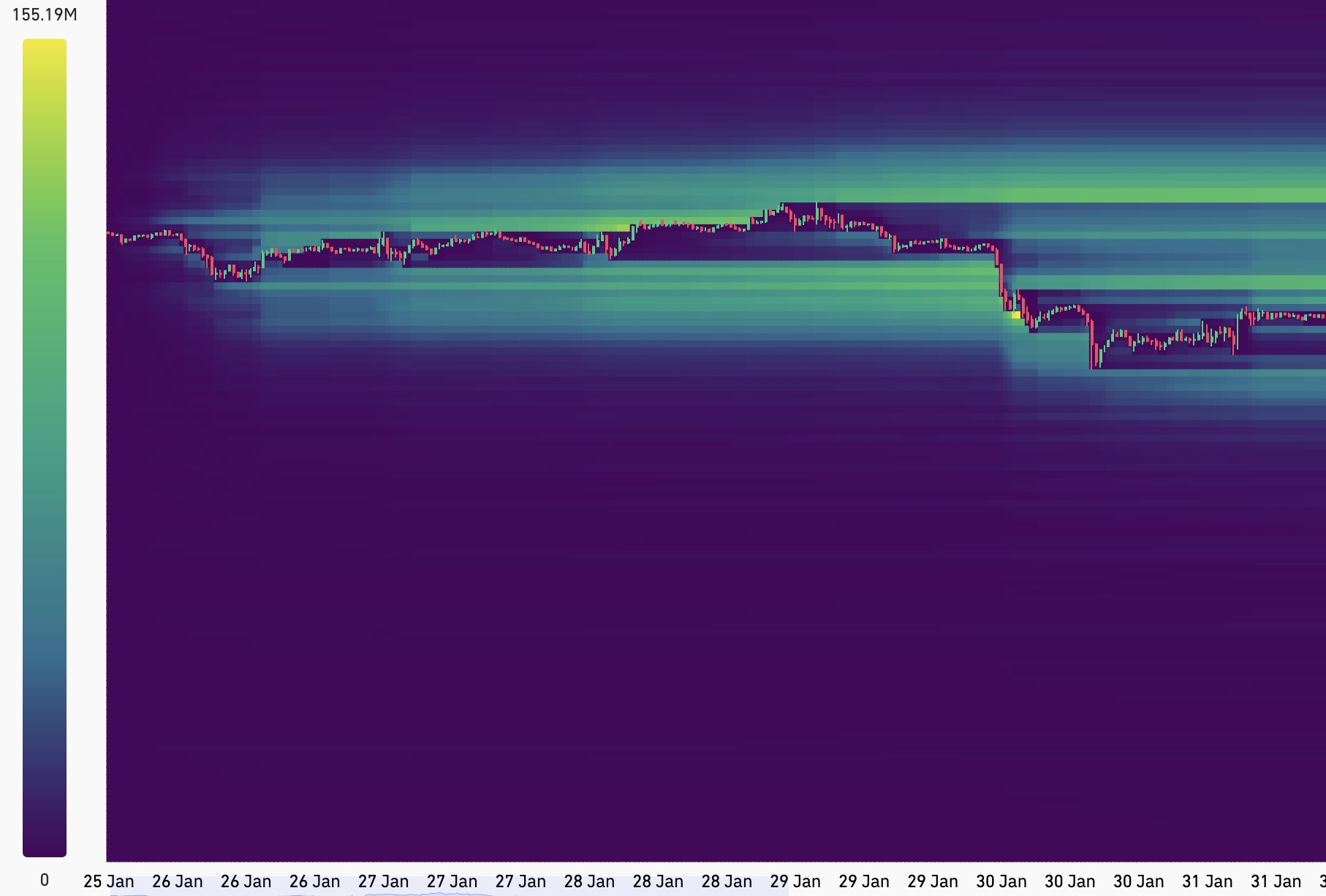

What a Liquidation Heatmap Represents

A liquidation heatmap aggregates estimated liquidation thresholds across derivatives venues. These thresholds are primarily composed of:

- Stop-loss orders placed by leveraged traders.

- Margin liquidation levels enforced by exchange risk engines.

- Forced deleveraging events when maintenance margin requirements are breached.

These orders are mechanical and automatic. They are not discretionary decisions made in real time, but deterministic outcomes of leverage, margin, and exchange rules.

When price enters a dense liquidity zone, execution is effectively guaranteed. The only variable is which participants are positioned to absorb that forced flow.