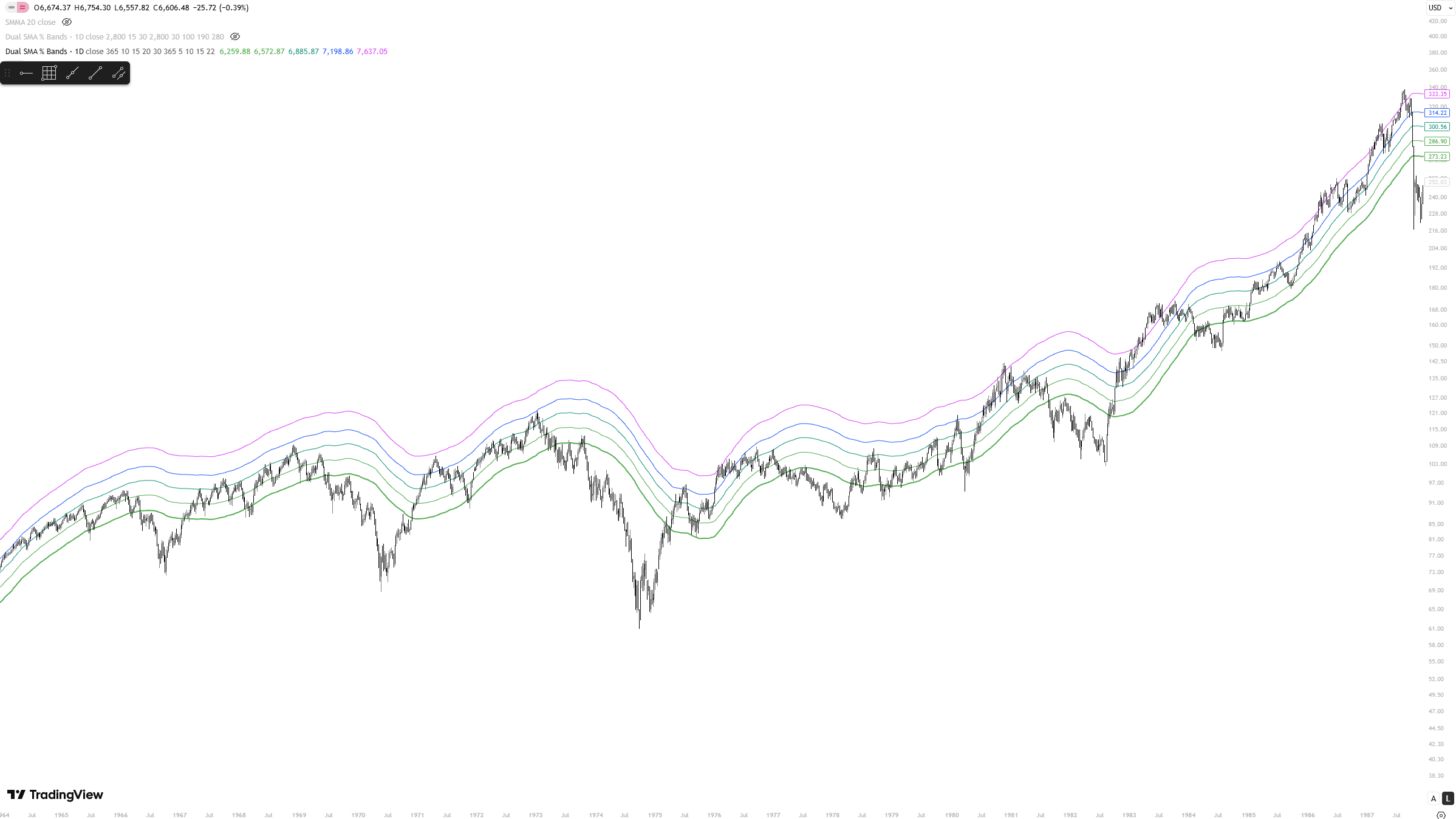

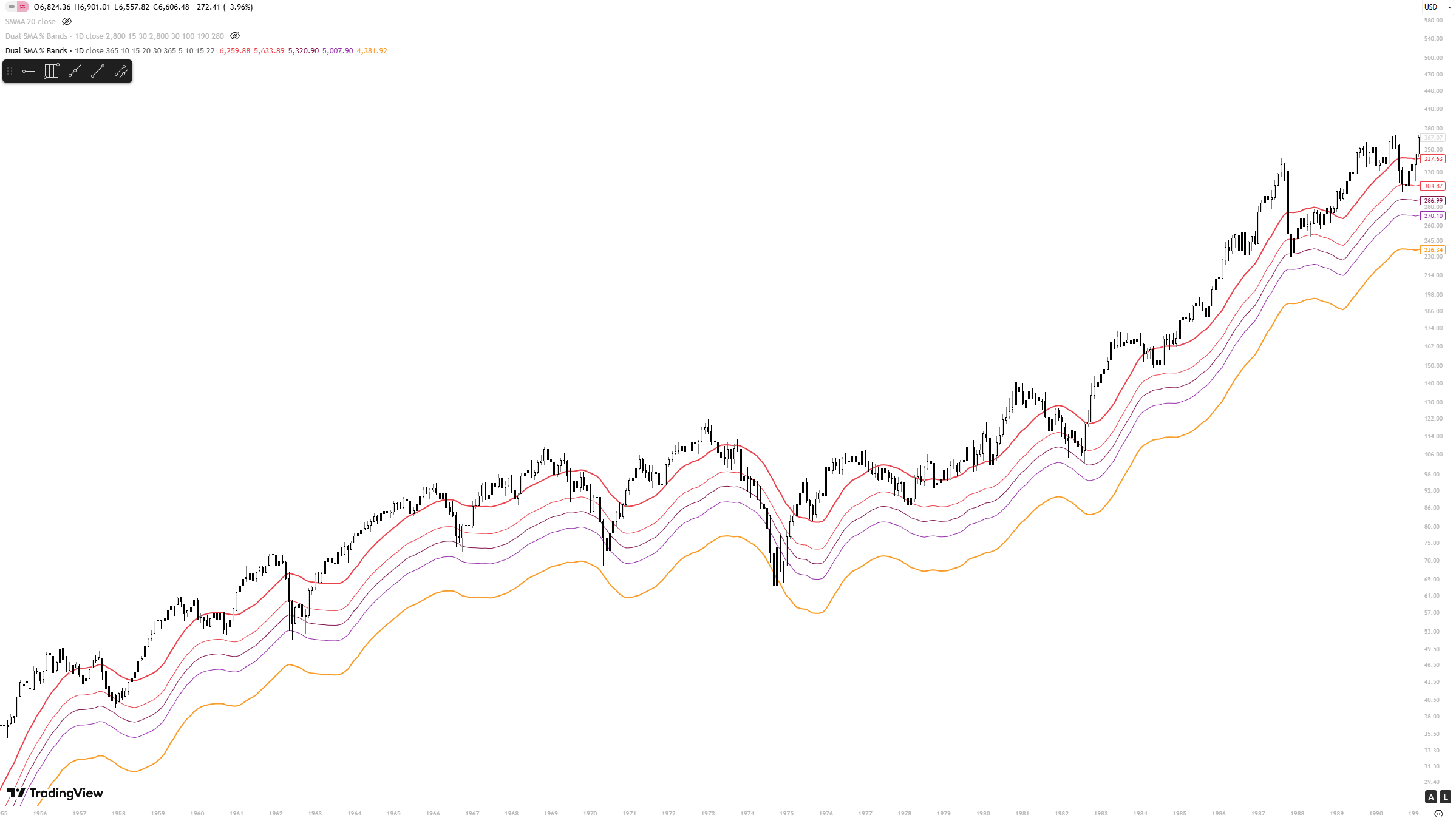

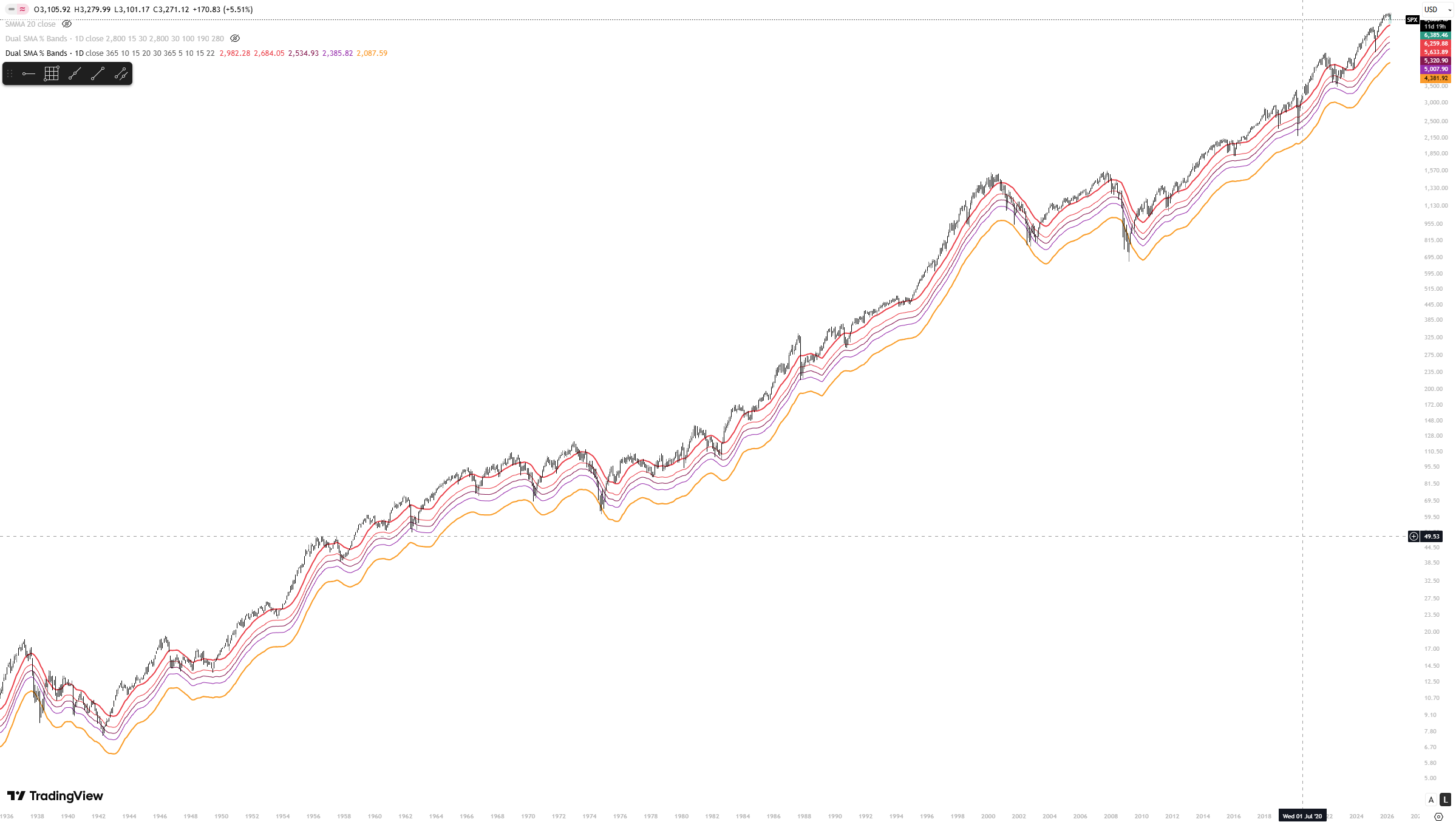

Section 1: Drawdown Bands

When the SPX trades below its 365-day mean, it enters zones where long-term risk has historically been skewed to the upside. The bands at 10%, 15%, 20%, and 30% below the yearly average define a tiered accumulation map, each level representing a progressively rarer dislocation from trend.

These are not buy signals. They are conditions that, across nearly nine decades of data, have consistently preceded above-average returns. The deeper the breach, the stronger the historical precedent. (Zoom in to view charts)

Across all regimes, the framework holds a consistent read: the 10-15% zone flags elevated long-term value; the 20-30% zone has marked generational entry conditions. In the post-2009 bull market, corrections have rarely breached the 15% band, making any such reading a significant signal going forward.